If you’ve been following private equity performance lately, you’ve probably noticed the headlines aren’t exactly glowing. Public markets have been on a tear since late 2022, leaving private equity returns looking decidedly underwhelming by comparison. Over the past three years, public equity has outperformed PE by a meaningful margin (8.2% versus 4.9% annualized returns).

For funds launched after 2020, the story gets even more challenging. These vintages are dealing with a perfect storm: high entry multiples, rising interest rates, and a macro environment that’s anything but forgiving. It’s enough to make even seasoned investors question whether something fundamental has shifted in private markets. But here’s the thing about private equity: three years doesn’t tell the whole story. And if history is any guide, the current performance gap might be setting up one of the better entry opportunities we’ve seen in years.

TL;DR: 5 Key Takeaways

- Historical patterns suggest patience pays off: PE funds from the 2008 crisis initially underperformed by 3.1% annually but ultimately delivered 2.1% excess returns over their full lifecycle.

- The opportunity universe keeps expanding: 85% of U.S. companies with $100M+ revenue remain privately held, while PE has grown 3x faster than public markets since 2000.

- Valuation arbitrage is real: Private companies are trading at meaningful discounts to public market multiples, creating compelling entry opportunities.

- Operational excellence becomes the new alpha: Success increasingly depends on genuine value creation rather than financial engineering.

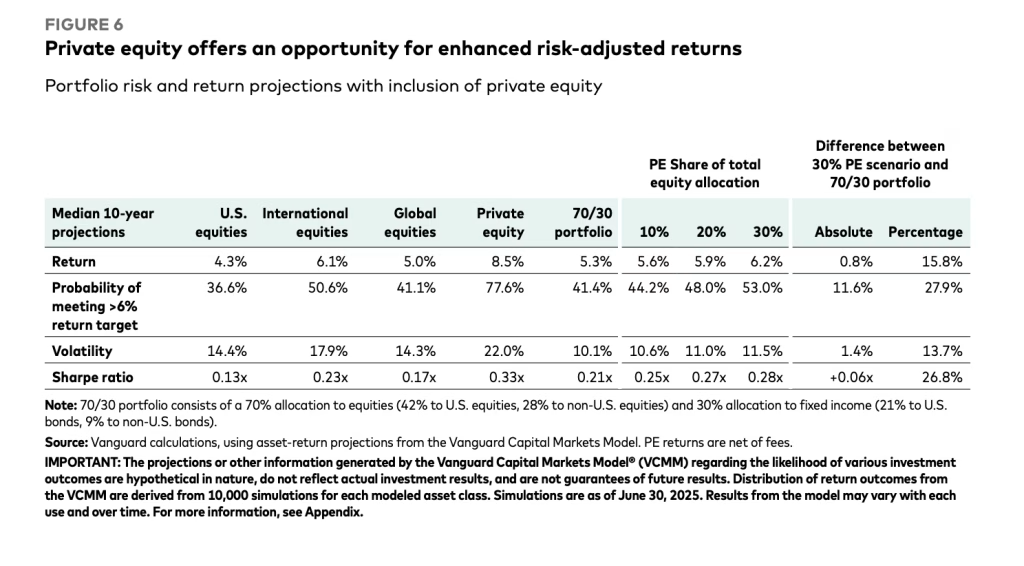

- The math still works for patient capital: Vanguard projects PE will outperform public markets by 350 basis points annually over the next decade.

The 2008 Playbook: Been Here Before

Let’s rewind to another period when PE looked like it was in serious trouble. During the 2008 financial crisis and its aftermath, PE funds launched between 2007-2012 got absolutely hammered in their early years. We’re talking about underperformance of 3.1% annually versus public markets (worse than what we’re seeing today).

The narrative back then was eerily similar: “PE is broken,” “The model doesn’t work in this environment,” “Public markets are the safer bet.” Sound familiar?

Fast forward to today, and those same “troubled” vintages ultimately outperformed public markets by 2.1% over their full lifecycle. The top-quartile managers did even better, delivering outsized returns that more than compensated for the rocky start. Private equity operates on a different timeline than public markets, and temporary dislocations often create the conditions for superior long-term performance.

The Opportunity Set Has Never Been Broader

While everyone’s focused on recent performance, something remarkable has been happening in private markets: the volume of opportunities has exploded. Since 2000, private equity has grown three times faster than public markets. Today, PE represents about 10% of global equity market capitalization (substantial, but hardly saturated). More importantly, 85% of U.S. companies generating over $100 million in revenue remain privately held. That’s an enormous pool of potential targets that simply doesn’t exist in public markets.

For strategic buyers and search funds, this expansion means more deal flow, more niche opportunities, and more chances to find that perfect acquisition target that others might miss. The depth and diversity of today’s private market ecosystem would have been unimaginable just two decades ago.

Are you ready to take advantage of these opportunities? Take this Buyer Readiness Self Test to make sure you’re positioned to win.

The Valuation Disconnect Creates Real Opportunities

Here’s where things get interesting from a tactical standpoint. While public market valuations, particularly in the U.S., remain elevated compared to historical norms, private company multiples look increasingly attractive. The valuation spread between public and private companies has exceeded historical averages, creating a genuine arbitrage opportunity. We’re seeing private companies trade at EV/EBITDA multiples significantly below their public market counterparts, even after accounting for the illiquidity discount.

For buyers with patience and the right operational expertise, this environment offers the chance to acquire quality assets at reasonable prices while public market investors chase momentum at peak valuations.

The Evolution from Financial Engineering to Real Value Creation

Perhaps the most important shift happening in PE isn’t about valuations or market timing; it’s about how returns are generated. The days of easy money through leverage and multiple expansion are largely behind us. Going forward, outperformance will increasingly depend on genuine operational improvements. This evolution actually favors sophisticated buyers who understand how to create value through operational excellence, strategic repositioning, and hands-on management support. It’s a higher bar, certainly, but it also creates sustainable competitive advantages for those who can clear it.

The PE firms thriving in this environment aren’t the ones relying on financial engineering tricks from the last cycle. They’re the ones rolling up their sleeves to genuinely improve the businesses they acquire, streamlining operations, expanding into new markets, upgrading technology, and building management capabilities.

The Math Still Works (If You Do It Right)

Despite all the recent noise, Vanguard’s latest capital markets projections remain bullish on private equity’s long-term prospects. They’re forecasting PE will outperform public markets by approximately 350 basis points annually over the next decade, a substantial premium that reflects the illiquidity and active risk that comes with private investing. Their models suggest a median 10-year return of 8.5% for global PE versus 5.0% for public equity. For investors who can handle the illiquidity and have access to quality managers, that’s a compelling value proposition.

The key phrase there is “quality managers.” Performance dispersion in PE has always been wide, and it’s likely to get wider in this more challenging environment. Success increasingly depends on three critical factors: partnering with proven operators, maintaining broad diversification across vintages and strategies, and sticking to a disciplined commitment program even when markets feel uncertain.

Forward Outlook

The current environment reminds us why private equity isn’t for everyone. It requires patience, sophistication, and the ability to see beyond short-term performance fluctuations. But for those who can navigate these requirements, the opportunity set remains compelling.

Market dislocations don’t last forever, but the businesses built during these periods often become the foundation of exceptional long-term returns. The firms positioning themselves thoughtfully in today’s market, focusing on operational value creation, maintaining disciplined valuations, and building diversified portfolios, are likely to look back on this period as a defining opportunity.

The three-year performance gap that has everyone concerned today may well become tomorrow’s setup for outperformance. In private equity, as in most things, timing matters less than time in the market.

Types of Independent Sponsors: How Fundless Sponsors Get Deals Done

Are you positioned to win? Find out.